Our bi-weekly Opinion provides you with latest updates and analysis on major capital market and financial investment industry issues.

Mobile Stock Trading by Retail Investors

Publication date Feb. 22, 2022

Summary

This article has analyzed listed stocks trading by 134,000 retail investors from March to October 2020 in Korea. According to the analysis result, mobile investors tend to have a higher turnover ratio and a larger day-trading proportion, buy stocks showing sharp price increases, and achieve poor performance, compared to investors using other trading platforms. Mobile stock trading by retail investors has been growing rapidly thanks to its benefits of greater accessibility and convenience. However, it also imposes costs such as irrational trading behaviors and poor investment performance. In this respect, it is necessary to prevent the accessibility and convenience of mobile trading systems from encouraging impulsive, speculative trading activities. Also, efforts should be exerted to create a mobile trading environment that can promote rational investment decisions.

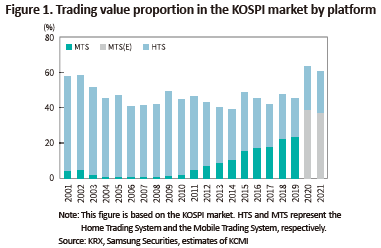

In Korea, direct stock trading has become prevalent among retail investors, which is well demonstrated by the 55.51 million active stock trading accounts and the 4.42 million IPO subscriptions attracted by LG Energy Solution. This trading boom is attributable to greater demand for stock investing and the spread of the Mobile Trading System (MTS) that has significantly improved accessibility and convenience for stock trading. MTS-based trading in Korea has continued growth since 2011, taking up 24% of the aggregate trading value in the KOSPI market in 2019 and nearly 40% in 2020 and 2021 (see Figure 1).

Since mobile trading is conducted on mobile phones, users of MTS can obtain investment information and engage in trading regardless of time and place. It usually offers a simple, intuitive user interface to take advantage of a small screen and provide less-experienced investors wider access to stock trading. Some studies have found that these benefits contribute to increasing the stock market participation of retail investors, but could adversely affect their investment performance and trading behaviors (Barber et al., 2021; Kalda et al., 2021). Empirically, retail investors have been observed to engage in stock trading more frequently, buy high-risk stocks and become more sensitive to short-term returns since the use of mobile trading platforms. This means they are highly likely to make impulsive, speculative investment decisions, rather than making a swift, rational response to changing market conditions. In view of the analysis, this article intends to examine what effects mobile trading would have on investment performance and trading behaviors by referring to listed stocks1) trading by around 134,000 investors during the period from March to October 2020.

Retail investors’ investment performance by platform

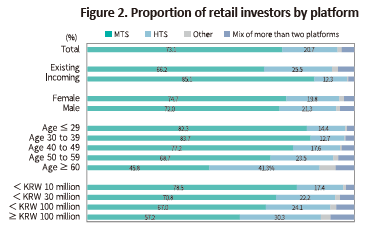

First, regarding the use of trading platforms by retail investors, the platforms are categorized into MTS, HTS (Home Trading System)2) and others (a brokerage’s branch or ARS). Investors whose trading value on a specific platform accounts for over 95% of the total can be defined as MTS-based investors, HTS-based investors and other investors. As illustrated in Figure 2, MTS-based investors and HTS-based investors represent 73.1% and 20.7% of the retail investors analyzed, respectively. Those who use more than two platforms account for 4.6% with other investors taking up just 1.6%.

In a classification of retail investors, the proportion of MTS-based investors is relatively higher among incoming investors,3) female investors, younger investors and those with a smaller amount of investment assets, compared to among existing investors, male investors, older investors and those with a larger amount of investment assets. Notably, the MTS-based investors represent 45.8% in investors aged 60 or older, and 57.2% in those with investment assets worth over KRW 100 million. Given this trend, Korea’s retail investors are rapidly shifting to MTS from HTS in terms of stock trading platforms.

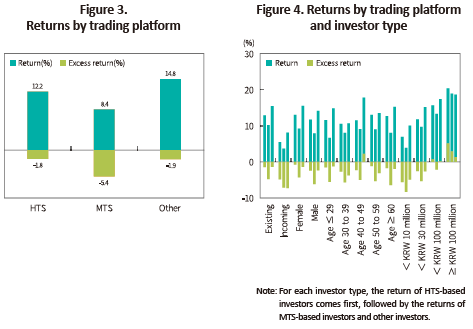

In a comparison of investment performance by platform, retail investors’ performance is measured by time-weighted returns of those who trade stocks for 20 days or longer during the analysis period and excludes transaction costs (trading fees and securities transaction tax). In Figure 3, MTS-based investors post an average 8.4% return, lower than 12.2% of HTS-based investors and 14.8% of other investors. Based on excess returns generated by deducting market returns4) from a given stock’s return during the trading period, MTS-based investors have an average excess return of -5.4%, achieving the lowest performance compared to -1.8% of HTS-based investors and -1.9% of other investors. The poor performance by MTS-based investors is hardly attributable to investor type compositions. In all retail investor groups classified by point of market entry, gender, age, and asset value, those using MTS fall behind HTS-based investors in terms of investment performance and such a difference in performance is statistically significant (see Figure 4).

This result suggests that mobile trading may encourage trading behaviors adversely affecting investment performance or retail investors who exhibit behaviors leading to poor performance may prefer trading stocks through mobile platforms. As a comparative analysis of the two potential causes requires a close examination, it is helpful to take a brief look at trading behaviors that are expected to undermine MTS-based investors’ performance.

Retail investors’ trading behaviors by platform

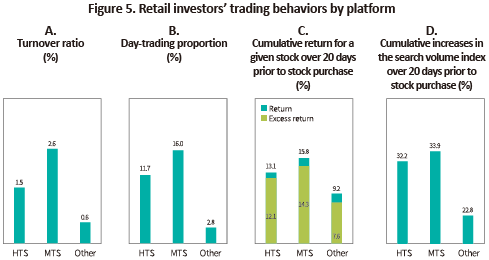

In Figure 5, A and B represent the average daily turnover ratio and the day-trading proportion by platform, respectively. The daily turnover ratio is calculated as the daily trading value (the average of buy and sell) divided by the portfolio value held by investors, whereas the day-trading proportion is derived by dividing the trading value—purchased and then sold on the same date—by the daily trading value. Compared to users of other platforms, MTS users have a higher daily turnover ratio and a larger day-trading proportion. The average daily turnover ratio of MTS-based investors stands at 2.6%, 1.7 times and 4.3 times higher than that of HTS-based investors and other investors, respectively. MTS-based investors reached 16.0% in the average day-trading proportion, 1.4 times and 5.7 times higher than that of HTS-based investors and other investors, respectively. This implies that users of MTS are more inclined to engage in speculative trading.

Figure 5’s C displays the cumulative return for a given stock over 20 days prior to the stock purchase. MTS-based investors’ cumulative return reaches 15.8% on average, higher than 13.1% of HTS-based investors and 9.2% of other investors. When compared based on excess returns, a similar trend has been delivered. MTS-based investors post 14.3% in excess return, the highest return level compared to HTS-based investors’ 12.1% and other investors’ 7.6%. This can be interpreted that MTS users are highly likely to buy stocks that show a sharp upward movement in prices.

In Figure 5, D indicates increases in the search volume index for a given stock over 20 days prior to the stock purchase. The search index refers to a normalized search volume of each stock based on data extracted from NAVER search trend,5) which helps measure market participants’ level of interest in stocks.6) Furthermore, in terms of an increase in the search volume index, MTS-based investors surpass other groups of investors by posting 33.9%, suggesting MTS users’ strong propensity to buy high-attention stocks. The results presented in Figure 5 are repeatedly shown in all retail investor groups classified by point of market entry, gender, age, and asset value.

Previous studies on investment performance and trading behaviors of retail investors have found that they tend to engage in excessive, speculative trading, pursue less-diversified portfolio, and prefer stocks that show a recent surge in returns or have noticeable characteristics. This trend is associated with behavioral biases such as sensation seeking, over-confidence, limited attention and representativeness biases, which serves as the leading cause of poor investment performance. The analysis of this article reveals that irrational trading behaviors and resultant weak performance have been more prominent in mobile trading.

Implications

MTS has become one of the most influential platforms for retail investors’ stock trading thanks to its benefits of accessibility and convenience. On the flip side, it also entails costs such as irrational trading behaviors and poor performance. Thus, it is necessary to contemplate how to improve retail investors’ mobile trading behaviors. If the mobile trading environment induces retail investors’ irrational behaviors, this should be urgently addressed. Likewise, if those engaging in irrational trading behaviors prefer using mobile platforms, it could give rise to problems.

Barber et al. (2021) have studied Robinhood users and come up with an interesting analysis. If a stock is included in the Top Mover list offered by the Robinhood app, Robinhood users are more likely to buy the stock, a phenomenon that has been hardly observed in investors using other platforms. This demonstrates that retail investors’ trading behavior can be swayed by the information provided by a stock trading app and the way the app displays specific information, implying that the mobile trading platform can be designed to guide retail investors toward rational investment activities.

More empirical and experimental research should be conducted to figure out which conditions are required to design a beneficial mobile trading platform. Considering irrational behaviors that have been identified until now, the fundamental direction is relatively obvious. The desirable approach is to put more focus on long-term return outlook and portfolio returns rather than on short-term return trends and returns on an individual stock. Also necessary is to raise awareness about the adverse impact of speculative, excessive trading activities by attracting more attention to and giving easy access to information regarding investment risks and transaction costs.

In the face of the uncertainty and complexity of stock trading, retail investors are susceptible to behavioral biases. It would be difficult to avoid irrational trading behaviors and resultant poor performance by focusing only on enhancing accessibility and convenience in mobile stock trading. In this respect, a proper mobile trading environment should be built to encourage retail investors to make rational trading decisions.

1) Stocks traded in the KONEX market and SPACs have been excluded from the analysis.

2) This includes the Web Trading System (WTS).

3) Incoming investors mean those who opened stock trading accounts after March 2020.

4) This refers to the KOSPI index- and the KOSDAQ index-weighted average returns.

5) https://datalab.naver.com/keyword/trendSearch.naver

6) The database created by Kim, Minki from KCMI has been used.

References

Barber, B. M., Huang, X., Odean, T., Schwarz, C., 2021, Attention induced trading and returns: Evidence from robinhood users, Journal of Finance , Forthcoming.

Kalda, A., Loos, B., Previtero, A., Hackethal, A., 2021, Smart (Phone) Investing? A within Investor-time Analysis of New Technologies and Trading Behavior, SAFE Working Paper No. 303, Available at SSRN: https://ssrn.com/abstract=3765652

Retail investors’ investment performance by platform

First, regarding the use of trading platforms by retail investors, the platforms are categorized into MTS, HTS (Home Trading System)2) and others (a brokerage’s branch or ARS). Investors whose trading value on a specific platform accounts for over 95% of the total can be defined as MTS-based investors, HTS-based investors and other investors. As illustrated in Figure 2, MTS-based investors and HTS-based investors represent 73.1% and 20.7% of the retail investors analyzed, respectively. Those who use more than two platforms account for 4.6% with other investors taking up just 1.6%.

In a classification of retail investors, the proportion of MTS-based investors is relatively higher among incoming investors,3) female investors, younger investors and those with a smaller amount of investment assets, compared to among existing investors, male investors, older investors and those with a larger amount of investment assets. Notably, the MTS-based investors represent 45.8% in investors aged 60 or older, and 57.2% in those with investment assets worth over KRW 100 million. Given this trend, Korea’s retail investors are rapidly shifting to MTS from HTS in terms of stock trading platforms.

This result suggests that mobile trading may encourage trading behaviors adversely affecting investment performance or retail investors who exhibit behaviors leading to poor performance may prefer trading stocks through mobile platforms. As a comparative analysis of the two potential causes requires a close examination, it is helpful to take a brief look at trading behaviors that are expected to undermine MTS-based investors’ performance.

In Figure 5, A and B represent the average daily turnover ratio and the day-trading proportion by platform, respectively. The daily turnover ratio is calculated as the daily trading value (the average of buy and sell) divided by the portfolio value held by investors, whereas the day-trading proportion is derived by dividing the trading value—purchased and then sold on the same date—by the daily trading value. Compared to users of other platforms, MTS users have a higher daily turnover ratio and a larger day-trading proportion. The average daily turnover ratio of MTS-based investors stands at 2.6%, 1.7 times and 4.3 times higher than that of HTS-based investors and other investors, respectively. MTS-based investors reached 16.0% in the average day-trading proportion, 1.4 times and 5.7 times higher than that of HTS-based investors and other investors, respectively. This implies that users of MTS are more inclined to engage in speculative trading.

Figure 5’s C displays the cumulative return for a given stock over 20 days prior to the stock purchase. MTS-based investors’ cumulative return reaches 15.8% on average, higher than 13.1% of HTS-based investors and 9.2% of other investors. When compared based on excess returns, a similar trend has been delivered. MTS-based investors post 14.3% in excess return, the highest return level compared to HTS-based investors’ 12.1% and other investors’ 7.6%. This can be interpreted that MTS users are highly likely to buy stocks that show a sharp upward movement in prices.

In Figure 5, D indicates increases in the search volume index for a given stock over 20 days prior to the stock purchase. The search index refers to a normalized search volume of each stock based on data extracted from NAVER search trend,5) which helps measure market participants’ level of interest in stocks.6) Furthermore, in terms of an increase in the search volume index, MTS-based investors surpass other groups of investors by posting 33.9%, suggesting MTS users’ strong propensity to buy high-attention stocks. The results presented in Figure 5 are repeatedly shown in all retail investor groups classified by point of market entry, gender, age, and asset value.

Implications

MTS has become one of the most influential platforms for retail investors’ stock trading thanks to its benefits of accessibility and convenience. On the flip side, it also entails costs such as irrational trading behaviors and poor performance. Thus, it is necessary to contemplate how to improve retail investors’ mobile trading behaviors. If the mobile trading environment induces retail investors’ irrational behaviors, this should be urgently addressed. Likewise, if those engaging in irrational trading behaviors prefer using mobile platforms, it could give rise to problems.

Barber et al. (2021) have studied Robinhood users and come up with an interesting analysis. If a stock is included in the Top Mover list offered by the Robinhood app, Robinhood users are more likely to buy the stock, a phenomenon that has been hardly observed in investors using other platforms. This demonstrates that retail investors’ trading behavior can be swayed by the information provided by a stock trading app and the way the app displays specific information, implying that the mobile trading platform can be designed to guide retail investors toward rational investment activities.

More empirical and experimental research should be conducted to figure out which conditions are required to design a beneficial mobile trading platform. Considering irrational behaviors that have been identified until now, the fundamental direction is relatively obvious. The desirable approach is to put more focus on long-term return outlook and portfolio returns rather than on short-term return trends and returns on an individual stock. Also necessary is to raise awareness about the adverse impact of speculative, excessive trading activities by attracting more attention to and giving easy access to information regarding investment risks and transaction costs.

In the face of the uncertainty and complexity of stock trading, retail investors are susceptible to behavioral biases. It would be difficult to avoid irrational trading behaviors and resultant poor performance by focusing only on enhancing accessibility and convenience in mobile stock trading. In this respect, a proper mobile trading environment should be built to encourage retail investors to make rational trading decisions.

1) Stocks traded in the KONEX market and SPACs have been excluded from the analysis.

2) This includes the Web Trading System (WTS).

3) Incoming investors mean those who opened stock trading accounts after March 2020.

4) This refers to the KOSPI index- and the KOSDAQ index-weighted average returns.

5) https://datalab.naver.com/keyword/trendSearch.naver

6) The database created by Kim, Minki from KCMI has been used.

References

Barber, B. M., Huang, X., Odean, T., Schwarz, C., 2021, Attention induced trading and returns: Evidence from robinhood users, Journal of Finance , Forthcoming.

Kalda, A., Loos, B., Previtero, A., Hackethal, A., 2021, Smart (Phone) Investing? A within Investor-time Analysis of New Technologies and Trading Behavior, SAFE Working Paper No. 303, Available at SSRN: https://ssrn.com/abstract=3765652