OPINION

2023 May/02

Crisis of Credit Suisse: Wipeout of Contingent Convertible (CoCo) Bonds and its Implications

May. 02, 2023

PDF

- Summary

- Amid the crisis of the global banking sector triggered by Silicon Valley Bank’s collapse, the bankruptcy risk faced by Credit Suisse (CS), a Global Systemically Important Bank, has come to the fore, causing much tension in the financial market. After having long struggled with risk management failures, lawsuits and penalties, CS has ended up being taken over by UBS under the intervention of the Swiss Financial Market Supervisory Authority (FINMA). During the takeover process, the writedown of contingent convertible (CoCo) bonds set off controversy and market confusion over the seniority between CoCo bonds and common equity. But it is safe to say that the restructuring of CS has been carried out speedily through a bail-in mechanism without any loss inflicted on depositors. In addition, the crisis of CS has shed light on the importance of banks’ risk management.

Considering Korean banks’ capital ratio, the possibility that CoCo bonds are written down or banking crises occur seems to be limited. However, as macroeconomic strains could persist, banks should strive to maintain market confidence while paying close attention to risk management and internal control. Notably, in the future, there may be restrictions on capital expansion using CoCo bonds, such as an increase in financing costs, which requires caution in managing the issuance size of CoCo bonds. The supervisory authorities need to revamp the regulatory system for capital requirements and recognize the importance of responding to market unrest in a rapid and orderly manner. Lastly, investors should be aware of an array of risks arising from investing in CoCo bonds, such as a principal writedown.

As risks mount in the global banking sector in the wake of Silicon Valley Bank (SBV)’s collapse, the crisis of Credit Suisse (CS)—widely regarded as being potentially insolvent—has come to the fore. Unlike SVB, CS acts as a Global Systemically Important Bank (G-SIB) and could have far-reaching effects on the global economy and systemic risk. Accordingly, the predicament of CS has raised concerns about a financial crisis, escalating volatility in the financial markets. As CS failed to turn around despite liquidity assistance from the Swiss financial regulator, the Swiss Financial Market Supervisory Authority (FINMA) engineered the takeover of CS by UBS. As part of the acquisition deal, its contingent convertible (CoCo) bonds were written down to zero. Against this backdrop, this article examines what went wrong at CS and how its CoCo bonds were written down, and discusses relevant implications.

Basel Ⅲ and CoCo bonds

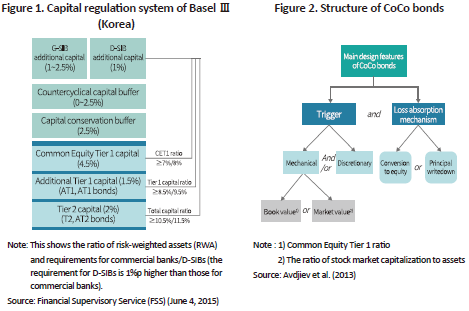

Basel Ⅲ, a regulatory framework for the banking sector developed in response to the global financial crisis, has adopted stricter criteria for capital expansion to improve banks’ loss absorption ability and limit the injection of public funds to a minimum level (BCBS, 2011a). Under the framework, the Financial Stability Board (FSB) and the Basel Committee on Banking Supervision (BCBS) have designated large banks whose failure could send shock waves through the global economy as G-SIBs and presented how to consistently manage systemic risk arising from G-SIBs by introducing tighter requirements for equity capital and liquidity. Korea’s financial authorities have also stepped up systemic risk monitoring by selecting domestic systemically important banks (D-SIBs).1) Figure 1 shows the capital regulation system of Basel Ⅲ.

Under Basel Ⅲ, CoCo bonds that are wiped out or converted to common equity if a bank runs into trouble can be recognized as Additional Tier 1 (AT1 for perpetual bonds) or Tier 2 (T2 for subordinated bonds), both of which are included in total capital separately from Common Equity Tier 1 (CET1).2) Accordingly, banks have issued CoCo bonds to shore up capital. The structure of CoCo bonds consists of the “loss absorption” mechanism and “trigger” activating the mechanism, with the aim of replenishing capital that is readily available in crisis times (Avdjiev et al., 2013, Figure 2). CoCo bonds can absorb losses through conversion to equity or a principal writedown, for which the trigger is determined by mechanical (pre-defined) requirements or the supervisory authority’s discretionary judgment. Mechanical triggers are classified by a selected index. The minimum CET1 is used as a book-value trigger while the minimum ratio of stock market capitalization to assets is used as a market-value trigger.3)

CoCo bonds with the risk of stock conversion or principal writedowns have been recognized as high-yield instruments, gaining popularity from investors in the low interest rate environment. In Korea, they have been sold to retail investors in the same way as banks’ trust instruments and securities firms’ retail bonds.4) As illustrated in the “Total Return Index” graph on the left side of Figure 3, the CoCo bond index recorded high cumulative returns before this round of banking crises occurred, which, however, suffered a big drop following the wipeout of Credit Suisse AT1 bonds. This suggests CoCo bond investors should be wary of risk factors such as a potential principal writedown and losses incurred from early redemption.

Credit Suisse’s crisis and CoCo bond wipeout

As the failure of SVB has sparked concerns about a bank run, struggles of the global banking sector have come to a head. In particular, concerns have been raised about the potential collapse of CS, which went through a crisis in 2022. Although the Swiss National Bank decided to provide emergency liquidity assistance of up to 50 billion francs (as of March 15), there was no sign of improvement as its CDS spreads jumped to more than 1,000bp. As a result, CS was taken over by UBS under the intervention of the Swiss government and FINMA on March 19 and during the takeover process, AT1 bonds (CoCo bonds) worth $17 billion (16 billion francs) were written down to zero. The wipeout of CS AT1 bonds is supposed to be triggered when the consolidated CET1 ratio of Credit Suisse Group falls below 7%; or FINMA orders CS to write down the bonds; or financial support from the public sector is required to prevent Credit Suisse Group from becoming insolvent or unable to pay its debts, or suffering any similar event.5) In a press release, FINMA made it clear that AT1 bonds issued by CS were written down in a “Viability Event” requiring government (or the public sector) assistance, which falls under the third category of the threshold above.6)

As part of the takeover deal, UBS promised to pay $3.25 billion to CS shareholders. But the Swiss government determined the complete writedown of AT1 bonds that typically rank higher than common equity on the hierarchy of claims, which set off controversy and heightened fears in the bond market. This resulted in a plunge in the value of AT1 bonds issued by banks (the graph on the right side of Figure 3). To quell the anxiety of investors, ECB Banking Supervision, Single Resolution Board (SRB) and European Banking Authority (EBA) announced a joint statement. The authorities said that “common equity acts as the first buffer for loss absorption and AT1 bonds should be written down only if common equity is entirely wiped out”, highlighting that the CS case is a one-off event.7) There are many issues to be resolved, such as AT1 bondholders’ possible legal action for the complete wipeout ordered by the Swiss regulator. However, the restructuring process of CS, one of the G-SIBs, has been carried out through a bail-in8) on a going concern basis, which seems to have alleviated the turmoil in the financial market.

In the aftermath of the crisis of CS, it is necessary to pay more attention to the importance of banks’ risk management than to the controversy over the seniority between AT1 bonds and common equity. The market lost its confidence in CS well before SVB collapsed. CS took a $7.2 billion loss from risk management failures such as Archegos fund and Greensill Capital incidents in 2021, faced various lawsuits and penalties arising from insufficient internal control, and showed chronic underperformance9) that continued from 2021. These worrying developments whipped up investors’ anxiety and led to capital outflows. As shown in Figure 4, CS saw an increase in CDS spreads, even starting from 2022. Although it raised the CET1 ratio to 14.1% by the end of 2022 through capital increase and carried out an overhaul,10) CS ended up with a crisis in a time of rising market volatility and mounting fears. It is noteworthy that, unlike the case of SVB, CS, a G-SIB, held a wide range of assets, liabilities and derivative positions. If banks like CS lose market confidence or suffer a credit rating downgrade, they are exposed to increased risk of capital outflows like a bank run and cannot engage in OTC derivatives or fund transactions,11) which, in turn, hinders normal business conduct and risk management and expands its vulnerability to market shocks. This underscores the importance of banks’ risk management and internal control in restoring and maintaining market confidence even at ordinary times. Meanwhile, BCBS or FSB is expected to overhaul the relevant regulatory regime, in light of recent bank runs, failed risk management by CS and market confusion about the writedown of CoCo bonds.

Wipeout threshold of Korean CoCo bonds and the current capital ratios of Korean banks and holding companies

Korean banks have issued CoCo bonds to shore up capital. Figure 5 illustrates the outstanding balance of Hybrid Tier 1 securities12) issued by banks and financial holding companies in Korea. The securities have grown considerably since 2017 and the outstanding value of the securities reached KRW 18.7 trillion for banks and 13.4 trillion for financial holding companies, respectively as of the end of 2022. Under the Act on the Structural Improvement of the Financial Industry, the writedown of Korean CoCo bonds will be triggered when an issuer is designated as an insolvent financial institution. Among various thresholds for the designation, the ratio of capital can be specified as total capital ratio of 4%, Tier 1 capital ratio of 3% and CET1 ratio of 2.3% (Article 42 of the Supervisory Regulation on Banking Business). This suggests Korea applies stricter terms to the writedown of AT1 bonds, compared to Europe with a bail-in mechanism.13)

As shown in Table 1, Korean banks seem to have a satisfactory capital ratio and thus, the possibility of CoCo bond writedown or a banking crisis is limited. However, the capital ratio declined in 2022 on a YoY basis and capital adequacy falls short of the levels of major economies.14) It should also be noted that the latest rise in interest rates and foreign exchange rates has raised uncertainties about the financial market and real economy.

Summary and Implications

The collapse of SVB has called attention to the crisis in the global banking sector. In particular, the potential failure of CS, one of G-SIBs, has sent jitters across the financial market. CS has long struggled with risk management failures and become susceptible to market shocks. As a result, it has been acquired by UBS, a move engineered by FINMA. As part of the takeover deal, its CoCo bonds, instead of common equity, were written down to zero, creating controversy and turmoil in the market. But it is safe to say that the restructuring of CS has been carried out speedily through a bail-in without any loss inflicted on depositors.

The debacle of CS offers the following implications. First of all, Korean banks’ solid capital ratio is unlikely to give rise to the potential writedown of CoCo bonds or a crisis in the banking sector. But as macroeconomic strains could persist, banks should strive to maintain market confidence while paying close attention to risk management and internal control. It is worth noting that concerns about bankruptcy could make banks more susceptible to market shocks. Notably, in the future, there may be restrictions on capital expansion using CoCo bonds, such as an increase in financing costs, which requires caution in managing the issuance size of CoCo bonds. The supervisory authorities need to revamp the regulatory regime for capital requirements15) and recognize the importance of responding to market unrest in a rapid and orderly manner. Lastly, investors should be aware of an array of risks arising from investing in CoCo bonds, such as a principal writedown and losses incurred from early redemption.

1) See BCBS (2011b). Depending on the bucket of G-SIBs, an additional capital requirement ranging from 1% to 2.5% is imposed. The financial authorities apply the additional requirement of 1% to Korean D-SIBs (Financial Supervisory Service, June 4, 2015).

2) For information on requirements for CET1, AT1 and T2 of Basel III framework, see BCBS (2011a). Specific requirements vary by country and matters concerning Korean banks can be found in annexes 3 and 3-5 of the Detailed Enforcement Regulations for Supervision of Banking Business.

3) As for European banks that actively issue CoCo bonds, the trigger point for CET1 stands at 5.125% (Low Trigger) or 7.0% (High Trigger).

4) Avdjiev et al. (2013) find that retail investors, private banks and asset management firms (funds) are major investors of CoCo bonds.

5) For writedown conditions for CoCo bonds and details about the writedown of CS, see Wi, J.W. & Kim, K. G. (2023) and Park, S.J. et al. (2023).

The exemplary term sheet of CS CoCo bonds: https://www.credit-suisse.com/about-us/en/investor-relations /financial-regulatory-disclosures/regulatory-disclosures/ capital- instruments.html

6) See https://www.finma.ch/en/news/2023/03/20230323-mm-at1-kapitalinstrumente/

7) Financial Times, March 21, 2023, Who killed Credit Suisse? Switzerland is not subject to the regulations of the EU in that the country is not part of the EU.

8) A bail-in is a financial relief mechanism adopted before a bail-out is set in motion. The mechanism helps a bank avoid failure by forcing its shareholders and creditors to share losses. With the wipeout of CoCo bonds, the loss of CS was passed on to creditors and the Swiss National Bank promised to provide UBS liquidity of up to $100 billion if needed as part of the takeover of CS.

9) Woori Finance Research Institute, November 11, 2022, A study on potential risk from the Credit Suisse crisis and relevant implications, chapter 2. In addition, a report of major flaws in the financial reporting of Credit Suisse was published by Woori Finance Research Institute on March 14, 2023.

10) Korea Center for International Finance, December 9, 2022, Capital expansion of Credit Suisse and assessment of its impact.

11) Financial services firms avoided transactions with CS to manage counterparty risk.

12) The item marked as Hybrid Tier 1 securities is used by this article. It is assumed to fall under the CoCo bond category as it is included capital items.

13) This implies CoCo bonds issued by European banks will reach the trigger point for writedowns earlier than those issued by Korean banks. For details on the threshold for designation as insolvent financial institutions and wipeout, see Park, S.J. et al (2023).

14) CET1 as of end-September 2022: 14.74% (EU), 15.65% (UK), 12.37% (US) and 12.26% (Korea) (Financial Services Commission and Financial Supervisory Service (March 16, 2023)).

15) The introduction of the countercyclical capital buffer and stress capital buffer was announced by Financial Services Commission and Financial Supervisory Service on March 16, 2023.

References

Basel Committee on Banking Supervision, 2011a, Basel III: A Global Regulatory Framework for More Resilient Banks and Banking Systems.

Basel Committee on Banking Supervision, 2011b, Global Systemically Important Banks: Assessment Methodology and the Additional Loss Absorbency Requirement.

Avdjiev, S., Kartasheva, A. V., Bogdanova, B., 2013, CoCos: a primer, BIS Quarterly Review September.

[Korean]

Financial Services Commission·Financial Supervisory Service, March 16, 2023, Reform of the financial prudence system to enhance banks’ loss absorption capability, press release.

Financial Supervisory Service, June 4, 2015, Plan for introducing domestic systemically important banks (D-SIBs) and regulations on bank holding companies, press release.

Financial Supervisory Service, March 30, 2023, BIS capital adequacy ratio of banks and bank holding companies as of end-December 2022, press release.

Park, S.J., Ji, H.S., Yun, K.H., Lee, K.W. and Song, K.J., March 24, 2023, Issues of the Credit Suisse crisis and review of the potential loss of Korean CoCo bonds, NICE Investors Service.

Wi, J.W. & Kim. K.G., March 21, 2023, Regarding the Credit Suisse AT1 Writedown Event, Korea Investors Service’s answer to concerns about the potential AT1 writedown in Korea, Korea Investors Service.

Basel Ⅲ and CoCo bonds

Basel Ⅲ, a regulatory framework for the banking sector developed in response to the global financial crisis, has adopted stricter criteria for capital expansion to improve banks’ loss absorption ability and limit the injection of public funds to a minimum level (BCBS, 2011a). Under the framework, the Financial Stability Board (FSB) and the Basel Committee on Banking Supervision (BCBS) have designated large banks whose failure could send shock waves through the global economy as G-SIBs and presented how to consistently manage systemic risk arising from G-SIBs by introducing tighter requirements for equity capital and liquidity. Korea’s financial authorities have also stepped up systemic risk monitoring by selecting domestic systemically important banks (D-SIBs).1) Figure 1 shows the capital regulation system of Basel Ⅲ.

Under Basel Ⅲ, CoCo bonds that are wiped out or converted to common equity if a bank runs into trouble can be recognized as Additional Tier 1 (AT1 for perpetual bonds) or Tier 2 (T2 for subordinated bonds), both of which are included in total capital separately from Common Equity Tier 1 (CET1).2) Accordingly, banks have issued CoCo bonds to shore up capital. The structure of CoCo bonds consists of the “loss absorption” mechanism and “trigger” activating the mechanism, with the aim of replenishing capital that is readily available in crisis times (Avdjiev et al., 2013, Figure 2). CoCo bonds can absorb losses through conversion to equity or a principal writedown, for which the trigger is determined by mechanical (pre-defined) requirements or the supervisory authority’s discretionary judgment. Mechanical triggers are classified by a selected index. The minimum CET1 is used as a book-value trigger while the minimum ratio of stock market capitalization to assets is used as a market-value trigger.3)

CoCo bonds with the risk of stock conversion or principal writedowns have been recognized as high-yield instruments, gaining popularity from investors in the low interest rate environment. In Korea, they have been sold to retail investors in the same way as banks’ trust instruments and securities firms’ retail bonds.4) As illustrated in the “Total Return Index” graph on the left side of Figure 3, the CoCo bond index recorded high cumulative returns before this round of banking crises occurred, which, however, suffered a big drop following the wipeout of Credit Suisse AT1 bonds. This suggests CoCo bond investors should be wary of risk factors such as a potential principal writedown and losses incurred from early redemption.

Credit Suisse’s crisis and CoCo bond wipeout

As the failure of SVB has sparked concerns about a bank run, struggles of the global banking sector have come to a head. In particular, concerns have been raised about the potential collapse of CS, which went through a crisis in 2022. Although the Swiss National Bank decided to provide emergency liquidity assistance of up to 50 billion francs (as of March 15), there was no sign of improvement as its CDS spreads jumped to more than 1,000bp. As a result, CS was taken over by UBS under the intervention of the Swiss government and FINMA on March 19 and during the takeover process, AT1 bonds (CoCo bonds) worth $17 billion (16 billion francs) were written down to zero. The wipeout of CS AT1 bonds is supposed to be triggered when the consolidated CET1 ratio of Credit Suisse Group falls below 7%; or FINMA orders CS to write down the bonds; or financial support from the public sector is required to prevent Credit Suisse Group from becoming insolvent or unable to pay its debts, or suffering any similar event.5) In a press release, FINMA made it clear that AT1 bonds issued by CS were written down in a “Viability Event” requiring government (or the public sector) assistance, which falls under the third category of the threshold above.6)

As part of the takeover deal, UBS promised to pay $3.25 billion to CS shareholders. But the Swiss government determined the complete writedown of AT1 bonds that typically rank higher than common equity on the hierarchy of claims, which set off controversy and heightened fears in the bond market. This resulted in a plunge in the value of AT1 bonds issued by banks (the graph on the right side of Figure 3). To quell the anxiety of investors, ECB Banking Supervision, Single Resolution Board (SRB) and European Banking Authority (EBA) announced a joint statement. The authorities said that “common equity acts as the first buffer for loss absorption and AT1 bonds should be written down only if common equity is entirely wiped out”, highlighting that the CS case is a one-off event.7) There are many issues to be resolved, such as AT1 bondholders’ possible legal action for the complete wipeout ordered by the Swiss regulator. However, the restructuring process of CS, one of the G-SIBs, has been carried out through a bail-in8) on a going concern basis, which seems to have alleviated the turmoil in the financial market.

In the aftermath of the crisis of CS, it is necessary to pay more attention to the importance of banks’ risk management than to the controversy over the seniority between AT1 bonds and common equity. The market lost its confidence in CS well before SVB collapsed. CS took a $7.2 billion loss from risk management failures such as Archegos fund and Greensill Capital incidents in 2021, faced various lawsuits and penalties arising from insufficient internal control, and showed chronic underperformance9) that continued from 2021. These worrying developments whipped up investors’ anxiety and led to capital outflows. As shown in Figure 4, CS saw an increase in CDS spreads, even starting from 2022. Although it raised the CET1 ratio to 14.1% by the end of 2022 through capital increase and carried out an overhaul,10) CS ended up with a crisis in a time of rising market volatility and mounting fears. It is noteworthy that, unlike the case of SVB, CS, a G-SIB, held a wide range of assets, liabilities and derivative positions. If banks like CS lose market confidence or suffer a credit rating downgrade, they are exposed to increased risk of capital outflows like a bank run and cannot engage in OTC derivatives or fund transactions,11) which, in turn, hinders normal business conduct and risk management and expands its vulnerability to market shocks. This underscores the importance of banks’ risk management and internal control in restoring and maintaining market confidence even at ordinary times. Meanwhile, BCBS or FSB is expected to overhaul the relevant regulatory regime, in light of recent bank runs, failed risk management by CS and market confusion about the writedown of CoCo bonds.

Wipeout threshold of Korean CoCo bonds and the current capital ratios of Korean banks and holding companies

Korean banks have issued CoCo bonds to shore up capital. Figure 5 illustrates the outstanding balance of Hybrid Tier 1 securities12) issued by banks and financial holding companies in Korea. The securities have grown considerably since 2017 and the outstanding value of the securities reached KRW 18.7 trillion for banks and 13.4 trillion for financial holding companies, respectively as of the end of 2022. Under the Act on the Structural Improvement of the Financial Industry, the writedown of Korean CoCo bonds will be triggered when an issuer is designated as an insolvent financial institution. Among various thresholds for the designation, the ratio of capital can be specified as total capital ratio of 4%, Tier 1 capital ratio of 3% and CET1 ratio of 2.3% (Article 42 of the Supervisory Regulation on Banking Business). This suggests Korea applies stricter terms to the writedown of AT1 bonds, compared to Europe with a bail-in mechanism.13)

As shown in Table 1, Korean banks seem to have a satisfactory capital ratio and thus, the possibility of CoCo bond writedown or a banking crisis is limited. However, the capital ratio declined in 2022 on a YoY basis and capital adequacy falls short of the levels of major economies.14) It should also be noted that the latest rise in interest rates and foreign exchange rates has raised uncertainties about the financial market and real economy.

Summary and Implications

The collapse of SVB has called attention to the crisis in the global banking sector. In particular, the potential failure of CS, one of G-SIBs, has sent jitters across the financial market. CS has long struggled with risk management failures and become susceptible to market shocks. As a result, it has been acquired by UBS, a move engineered by FINMA. As part of the takeover deal, its CoCo bonds, instead of common equity, were written down to zero, creating controversy and turmoil in the market. But it is safe to say that the restructuring of CS has been carried out speedily through a bail-in without any loss inflicted on depositors.

The debacle of CS offers the following implications. First of all, Korean banks’ solid capital ratio is unlikely to give rise to the potential writedown of CoCo bonds or a crisis in the banking sector. But as macroeconomic strains could persist, banks should strive to maintain market confidence while paying close attention to risk management and internal control. It is worth noting that concerns about bankruptcy could make banks more susceptible to market shocks. Notably, in the future, there may be restrictions on capital expansion using CoCo bonds, such as an increase in financing costs, which requires caution in managing the issuance size of CoCo bonds. The supervisory authorities need to revamp the regulatory regime for capital requirements15) and recognize the importance of responding to market unrest in a rapid and orderly manner. Lastly, investors should be aware of an array of risks arising from investing in CoCo bonds, such as a principal writedown and losses incurred from early redemption.

1) See BCBS (2011b). Depending on the bucket of G-SIBs, an additional capital requirement ranging from 1% to 2.5% is imposed. The financial authorities apply the additional requirement of 1% to Korean D-SIBs (Financial Supervisory Service, June 4, 2015).

2) For information on requirements for CET1, AT1 and T2 of Basel III framework, see BCBS (2011a). Specific requirements vary by country and matters concerning Korean banks can be found in annexes 3 and 3-5 of the Detailed Enforcement Regulations for Supervision of Banking Business.

3) As for European banks that actively issue CoCo bonds, the trigger point for CET1 stands at 5.125% (Low Trigger) or 7.0% (High Trigger).

4) Avdjiev et al. (2013) find that retail investors, private banks and asset management firms (funds) are major investors of CoCo bonds.

5) For writedown conditions for CoCo bonds and details about the writedown of CS, see Wi, J.W. & Kim, K. G. (2023) and Park, S.J. et al. (2023).

The exemplary term sheet of CS CoCo bonds: https://www.credit-suisse.com/about-us/en/investor-relations /financial-regulatory-disclosures/regulatory-disclosures/ capital- instruments.html

6) See https://www.finma.ch/en/news/2023/03/20230323-mm-at1-kapitalinstrumente/

7) Financial Times, March 21, 2023, Who killed Credit Suisse? Switzerland is not subject to the regulations of the EU in that the country is not part of the EU.

8) A bail-in is a financial relief mechanism adopted before a bail-out is set in motion. The mechanism helps a bank avoid failure by forcing its shareholders and creditors to share losses. With the wipeout of CoCo bonds, the loss of CS was passed on to creditors and the Swiss National Bank promised to provide UBS liquidity of up to $100 billion if needed as part of the takeover of CS.

9) Woori Finance Research Institute, November 11, 2022, A study on potential risk from the Credit Suisse crisis and relevant implications, chapter 2. In addition, a report of major flaws in the financial reporting of Credit Suisse was published by Woori Finance Research Institute on March 14, 2023.

10) Korea Center for International Finance, December 9, 2022, Capital expansion of Credit Suisse and assessment of its impact.

11) Financial services firms avoided transactions with CS to manage counterparty risk.

12) The item marked as Hybrid Tier 1 securities is used by this article. It is assumed to fall under the CoCo bond category as it is included capital items.

13) This implies CoCo bonds issued by European banks will reach the trigger point for writedowns earlier than those issued by Korean banks. For details on the threshold for designation as insolvent financial institutions and wipeout, see Park, S.J. et al (2023).

14) CET1 as of end-September 2022: 14.74% (EU), 15.65% (UK), 12.37% (US) and 12.26% (Korea) (Financial Services Commission and Financial Supervisory Service (March 16, 2023)).

15) The introduction of the countercyclical capital buffer and stress capital buffer was announced by Financial Services Commission and Financial Supervisory Service on March 16, 2023.

References

Basel Committee on Banking Supervision, 2011a, Basel III: A Global Regulatory Framework for More Resilient Banks and Banking Systems.

Basel Committee on Banking Supervision, 2011b, Global Systemically Important Banks: Assessment Methodology and the Additional Loss Absorbency Requirement.

Avdjiev, S., Kartasheva, A. V., Bogdanova, B., 2013, CoCos: a primer, BIS Quarterly Review September.

[Korean]

Financial Services Commission·Financial Supervisory Service, March 16, 2023, Reform of the financial prudence system to enhance banks’ loss absorption capability, press release.

Financial Supervisory Service, June 4, 2015, Plan for introducing domestic systemically important banks (D-SIBs) and regulations on bank holding companies, press release.

Financial Supervisory Service, March 30, 2023, BIS capital adequacy ratio of banks and bank holding companies as of end-December 2022, press release.

Park, S.J., Ji, H.S., Yun, K.H., Lee, K.W. and Song, K.J., March 24, 2023, Issues of the Credit Suisse crisis and review of the potential loss of Korean CoCo bonds, NICE Investors Service.

Wi, J.W. & Kim. K.G., March 21, 2023, Regarding the Credit Suisse AT1 Writedown Event, Korea Investors Service’s answer to concerns about the potential AT1 writedown in Korea, Korea Investors Service.